RTI Submissions Explained: What UK Employers Must File (FPS & EPS)

RTI Submissions Explained: What UK Employers Must File (FPS & EPS)

If you employ staff in the UK, understanding your payroll reporting obligations is essential for running a legally compliant business. Gone are the days of sending a single end-of-year return to the taxman. Under the Real Time Information (RTI) system, employers must report payroll data to HM Revenue & Customs (HMRC) every time they pay their employees.

The primary purpose of RTI submissions is to ensure that HMRC receives accurate, up-to-date information regarding income tax, National Insurance contributions, and other deductions. This continuous flow of data allows the government to adjust tax codes quickly and calculate state benefits accurately.

To stay compliant, there are two main submission types that employers file regularly: the Full Payment Submission (FPS) and the Employer Payment Summary (EPS). This guide provides everything you need to know about navigating these crucial documents.

What Is an RTI Payment Submission?

A payment submission is a digital report sent directly to HMRC that details exactly what you have paid your employees and the deductions you have made. For PAYE reporting, this creates a clear, transparent record of your company's tax liabilities.

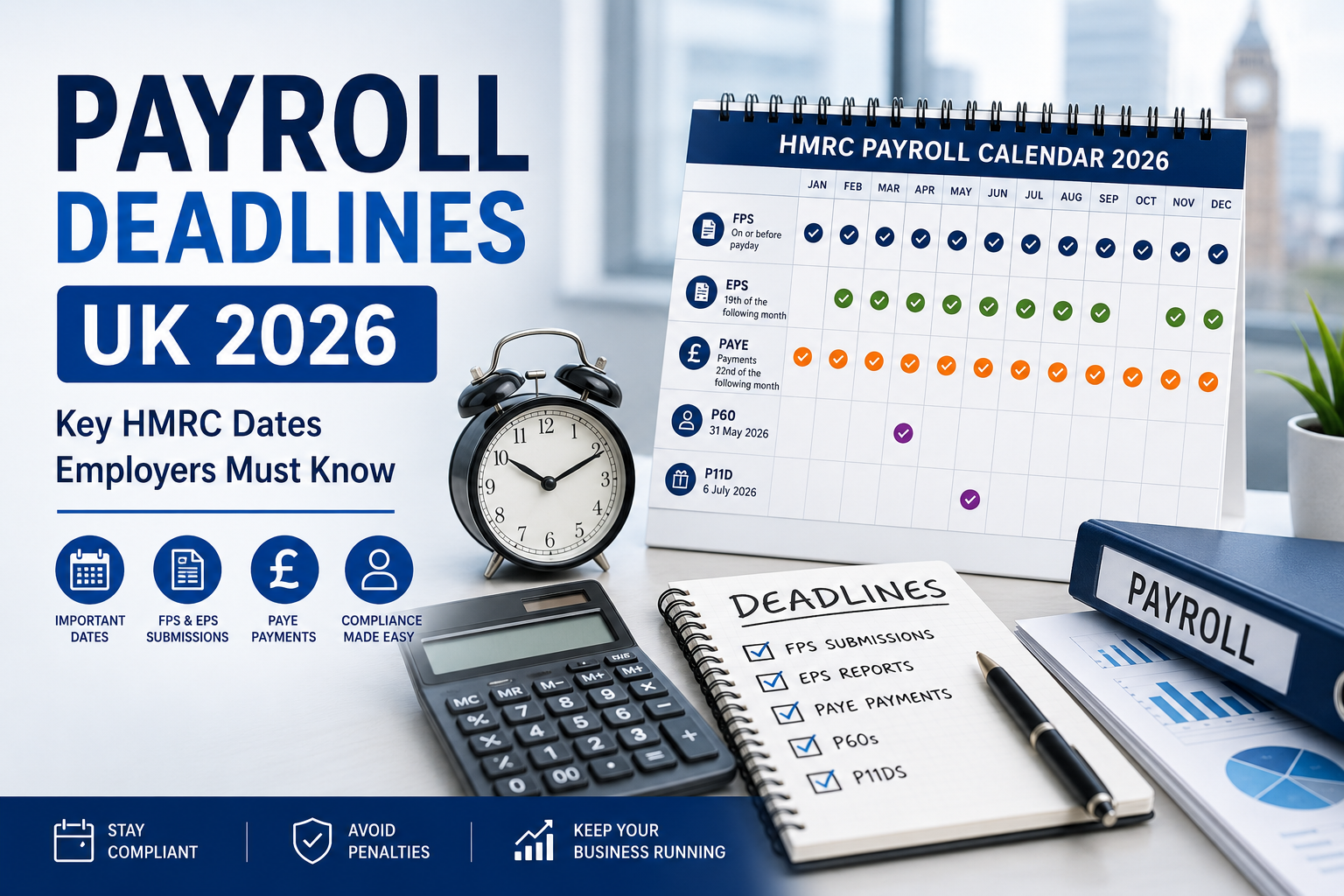

The legal timing requirement for these submissions is strict. You must submit your payment submission on or before the day you pay your employees. Failing to inform HMRC on time leads to severe penalties, making it vital to understand the mechanics of both the FPS and the EPS.

Full Payment Submission (Full Payment Submission FPS) — What Employers Must File

The Full Payment Submission FPS is the heartbeat of your payroll compliance. The role of the Full Payment Submission is to inform HMRC about the payments and deductions made to your employees during a specific pay period.

You must remember a simple rule: an FPS is required every time employees are paid. Whether you pay your staff weekly, fortnightly, or monthly, a regular FPS must accompany the payment. This submission drives the calculations for your PAYE liability, telling HMRC exactly how much income tax and National Insurance you owe them for that period.

When To Submit An FPS

The golden rule of running payroll is to submit the FPS on or before the employee payday. If your staff receive their wages in their bank accounts on the 25th of the month, HMRC must receive the FPS by the 25th at the latest.

To avoid missing these critical payment dates, we strongly advise you to automate recurring payday submissions. Most modern payroll software allows you to schedule your FPS and EPS submissions, reducing the risk of human error and late filing penalties.

What Payroll Data To Include On An FPS

A compliant FPS contains specific payroll data. HMRC relies on this information to match the payment to the correct individual. You must require the employee name as submitted to HMRC—nicknames or shortened names can cause mismatches in the HMRC records.

You also require National Insurance number verification for every worker. Furthermore, the FPS must accurately report the current tax code and the pay-to-date amounts for the relevant tax year. If these details are incorrect, the employee may pay the wrong amount of tax.

Starters: Reporting New Employee Details

When new employees join your business, you must report their details accurately on your next submission. You should capture new employee starter checklist responses meticulously. If the new employee provides a P45 from their previous employer, you must include the P45 details in the FPS. This ensures their tax details carry over seamlessly, preventing them from being placed on an emergency tax code unnecessarily.

Leavers: Marking Final Submission

When an employee leaves your business, you do not need to send a separate form to HMRC. Instead, you simply mark the employee as a leaver on their final FPS. You must include their leaving date on this final submission date. Once processed, you then generate a P45 to give to the departing employee.

Employer Payment Summary (Employer Payment Summary EPS) And EPS Submissions

While the FPS tells HMRC how much tax you have deducted, the Employer Payment Summary EPS tells them about any reductions you are claiming against that tax bill. The primary purpose of the Employer Payment Summary is to report adjustments that lower your overall PAYE liability.

EPS submissions adjust the FPS-calculated liabilities by applying statutory reclaims and allowances. Without the EPS, HMRC will expect you to pay the full amount calculated from your FPS data.

When You Need To Submit An EPS

You do not necessarily need to submit an EPS every single tax month. However, you must submit an EPS if you are reclaiming statutory payments, such as statutory sick pay, statutory maternity pay, or statutory adoption pay.

You also need to submit an EPS to claim the Employment Allowance, which reduces your employer National Insurance liability. Finally, you require a nil EPS when no payments were made to any employees during a tax month. The deadline to submit an EPS is the 19th of the following tax month.

Common Reasons For EPS Submissions

The most common reasons for filing an EPS involve claiming money back or reporting specific reductions. These include:

- Reporting CIS deductions suffered (if your business operates in the construction industry and a contractor has withheld tax from your payments).

- Claiming statutory pay recoveries, such as reclaiming a portion of statutory maternity pay from the government.

- Reporting a NIC holiday or regional NIC deductions.

- Making an Employment Allowance claim.

By submitting an EPS, you ensure that the amount you actually pay HMRC accurately reflects your true PAYE position after these statutory payments recovered and deductions suffered are applied.

EPS Submission Via Payroll Software Or HMRC Account

There are two main ways to file an EPS. We highly recommend using payroll software to file your EPS submissions. Integrated payroll systems calculate your statutory pay and Employment Allowance automatically, creating the EPS in the background.

Alternatively, if you manage a very small payroll system, you can log into your HMRC account for manual filing using the Basic PAYE Tools. Whichever method you choose, you must save the EPS submission confirmations from your HMRC account to prove you met your obligations.

Using Payroll Software To Automate RTI Submissions

The complexities of rti submissions explained what uk employers must file fps and eps highlight the need for robust digital tools. We strongly recommend using HMRC-recognised payroll software.

A reliable software package streamlines your payroll compliance. You should instruct the system to enable automatic FPS filing on payday. Furthermore, advise your payroll team to schedule monthly EPS checks in the software before the 19th of the month. By letting the software do the heavy lifting, you significantly reduce the administrative burden on your business.

Payroll Data Quality And Payroll Compliance

Submitting an FPS or EPS is only part of the battle; the data inside those submissions must be flawlessly accurate. Poor data quality leads to incorrect tax codes, underpaid staff, and frustrated employees.

To maintain excellent payroll compliance, verify employee details before each payroll run. Reconcile your payroll data to your accounting records to ensure every penny is accounted for. Furthermore, UK employers must retain payroll records for the required statutory period (usually three years from the end of the tax year they relate to). We advise business owners to review payroll compliance procedures quarterly to identify and correct any systemic errors.

Corrections, Nil Returns And Final Submission Procedures

Mistakes happen, but HMRC provides clear mechanisms for fixing them. If you realise you have made an error on a previous submission, you must explain sending a corrected FPS or EPS for the period as soon as possible. Most payroll software allows you to submit an updated FPS that overwrites the previous data for that specific pay period.

If you have a period where no staff are paid, perhaps because your business is seasonal, you cannot simply stay silent. You must instruct your team to submit a nil EPS for inactive pay periods. This informs HMRC that no payment is due, stopping them from estimating a charge and issuing a penalty.

Finally, at the end of the tax year (5 April), you must outline steps for making a final submission for the tax year. This involves marking your last FPS or EPS of the year as the "final submission for the tax year", which signals to HMRC that your payroll reporting for that year is complete.

Penalties, Recordkeeping And HMRC Account Checks

HMRC does not treat late submissions lightly. You must understand the late-filing penalty risk associated with both the FPS and EPS. If you fail to submit your FPS on or before payday, or your EPS by the 19th of the following tax month, you may face automatic financial penalties. These fines scale based on the number of employees you have.

To protect your business, always keep proof of submissions for disputes. If HMRC claims a submission was late, a digital confirmation receipt is your best defence. Additionally, instruct your payroll team to check RTI notices in your HMRC account regularly. This dashboard provides crucial updates on your PAYE scheme, alerts you to new tax codes, and flags any outstanding liabilities or late filing penalties.

Practical Checklist: What Employers Must File Each Pay Period

To help you stay compliant and avoid unnecessary stress, follow this practical checklist every single time you process employee pay:

- Update employee details: Ensure all new starters are added with correct National Insurance numbers and P45 details. Mark any leavers appropriately.

- Calculate pay and deductions: Double-check income tax, National Insurance, and other deductions like student loans or pension contributions.

- File an FPS for every pay run where payments occur: Submit this to HMRC on or before the day you pay staff.

- Identify adjustments: Check if you need to report CIS deductions suffered or reclaim statutory payments (like statutory sick pay or statutory adoption pay).

- File an EPS when adjustments or reclaims are needed: Submit this by the 19th of the following tax month.

- Submit a nil EPS if no payments occurred in the period: Never leave HMRC guessing if your payroll is temporarily inactive.

- Keep payroll software and HMRC account credentials updated: Ensure your systems are running the latest tax tables and that your login details are secure.

Managing your RTI submissions, from the regular FPS to the complex Employer Payment Summary EPS, is a demanding task. However, by establishing a clear payroll routine and leveraging modern software, UK employers can navigate the system with confidence.

If you find running payroll is taking up too much of your valuable time, or you are worried about late filing penalties, professional help is available. We can manage your complete PAYE scheme, ensuring every FPS and EPS is submitted flawlessly and on time.

Ready to remove the stress of RTI submissions and ensure total compliance? Visit our payroll services page today to discover how our expert team can support your business.

Get in touch today to see how we can help you!

Contact us

.png)

-min.png)

.png)