Payroll Deadlines UK 2026: Key HMRC Dates Employers Must Know

Payroll Deadlines UK 2026: Key HMRC Dates Employers Must Know

Missing a payroll deadline can trigger penalties, interest charges, rushed corrections, and frustrated employees. For UK employers and payroll teams, 2026 brings the usual year-end filing pressure alongside several important legislative changes, so getting your calendar right matters more than ever.

This guide explains the main payroll deadlines UK employers need to know for the end of the 2025/26 tax year and the start of the 2026/27 tax year. It covers what to file, when to file it, how the Full Payment Submission (FPS) and Employer Payment Summary (EPS) work, and which changes may affect your payroll settings from April 2026.

If you would prefer professional support with payroll deadlines, RTI submissions and HMRC compliance, our payroll services can help keep everything accurate and on time.

Who This Guide Is For

This guide is written for UK employers, finance teams, HR teams, and payroll professionals who run payroll through PAYE and Real Time Information (RTI).

If you run payroll in-house, this guide will help you plan your deadlines and checks. If you work with an outsourced provider, it will help you monitor what should be filed and when.

Why Payroll Deadlines Matter

Payroll deadlines are not just admin dates. They affect compliance, cash flow, employee confidence, and reporting accuracy across the tax year.

HMRC can charge penalties for late RTI reports and late PAYE payments. Interest can also apply, increasing the cost of missing a deadline. Where late payment continues, further penalties may follow after 6 months and 12 months.

If payroll errors continue or records are poor, employers can also spend more time dealing with corrections and year-end reporting.

For a deeper look at error prevention, read our guide to payroll mistakes that trigger HMRC penalties.

Key Dates Around The End Of The 2025/26 Tax Year

The end of the 2025/26 tax year is one of the busiest points in the payroll calendar. The main deadline is 5 April 2026, which marks the end of the tax year.

Around this point, employers should:

- Finalise the last payroll for the year

- Check starters and leavers

- Confirm tax codes and payroll benefits treatment

- Reconcile PAYE, Income Tax and National Insurance figures

- Prepare the final submission to HMRC

- Record P32 and payment details

- Plan P60 distribution

5 April 2026: End Of The 2025/26 Tax Year

5 April 2026 is the last day of the 2025/26 tax year. This date closes the final pay period for the year and should be included in every payroll calendar.

Before or on this date, employers should:

- Complete the last payroll run for the 2025/26 tax year

- Confirm employee records are up to date

- Review leavers, starters and irregular payments

- Check National Insurance category letters

- Ensure payroll benefits and salary sacrifice arrangements are reflected correctly

- Reconcile payroll totals against internal reports and the P32

This is also the point to confirm whether you need an FPS, an EPS, or both for the final pay period.

6 April 2026: Start Of The 2026/27 Tax Year

The new tax year starts on 6 April 2026. From that point, employers need to apply updated payroll settings, rates and thresholds before the first pay period is processed.

At the start of the new tax year, employers should:

- Update payroll software for new tax tables

- Carry forward tax codes in line with HMRC P9X guidance

- Confirm National Insurance thresholds

- Check statutory payment rates

- Review State Pension age changes for affected employees

- Update student loan plan settings where required

You can check current employer rates and thresholds on the official GOV.UK rates and thresholds for employers page.

Full Payment Submission: What It Is And When To Send It

The Full Payment Submission, or FPS, is the main RTI return used to report pay and deductions to HMRC. It includes pay, Income Tax, National Insurance contributions, student loan deductions, statutory payments and other payroll information for each employee.

The key rule for FPS filing is simple: you must submit the FPS on or before the date you pay employees.

This applies whether you run monthly payroll, weekly payroll or another pay frequency. The filing deadline is linked to payday, not month-end.

For a more detailed explanation, read our guide to RTI submissions, FPS and EPS.

Final FPS For The Tax Year

For the final pay period in the 2025/26 tax year, the FPS should include the final submission indicator if it is your last submission for the year.

Before sending the final submission, check:

- All employee pay for the tax year has been included

- Leavers are marked correctly

- Year-to-date figures reconcile

- Payroll benefits and deductions are correct

- No further payment submission is due for that year

Employer Payment Summary: When It Is Used

The Employer Payment Summary, or EPS, is used when the employer needs to adjust what is due to HMRC or report that no employees were paid in a tax month.

You may need to send an EPS when:

- No payments were made to employees in a tax month

- You are reclaiming statutory payment recoveries

- You need to report apprenticeship levy amounts

- You are claiming Small Employers' Relief

- CIS payments or other adjustments apply

When To Send A No-Pay EPS

If no employees are paid in a tax month, the employer should send a no-pay EPS by the 19th of the following month. This tells HMRC no payment submission was due for that period.

Missing an EPS can lead HMRC to assume PAYE is due, which can create avoidable chasing activity and confusion.

Monthly PAYE Payments And National Insurance Contributions

PAYE responsibilities do not end with filing. Employers must also pay HMRC on time.

For most employers paying electronically, the payment deadline is the 22nd of the following month. If the 22nd falls on a weekend or bank holiday, payment should clear on the last working day before it.

This applies to PAYE liabilities including:

- Income Tax deducted from employees

- Employee and employer National Insurance contributions

- Student loan deductions

- Other regular payroll deductions due through PAYE

You can also review AccountingPreneur’s National Insurance contributions resource for wider guidance.

Monthly Payment Deadlines

If you pay monthly, your typical cycle is:

- Payroll processed during the tax month

- FPS submitted on or before payday

- EPS submitted by the 19th where required

- PAYE and National Insurance paid by the 22nd if paying electronically

For official deadline guidance, see GOV.UK guidance on reporting payroll information to HMRC.

How To Reduce Late Payment Penalties

To reduce the risk of late PAYE payments and interest charges:

- Set internal cut-off dates before each payroll run

- Approve payroll earlier where bank holidays affect processing

- Monitor bank file release times

- Reconcile your P32 after each pay period

- Check that funds will clear by the HMRC deadline

P60s, P11Ds And Other Year-End Dates

Several key dates fall soon after the end of the tax year. These should be treated as fixed compliance dates.

31 May 2026: P60 Deadline

Employers must issue a P60 to every employee who was employed on 5 April 2026 by 31 May 2026.

The P60 shows the employee’s pay, Income Tax and National Insurance totals for the tax year. It must be accurate and based on final filed payroll data.

6 July 2026: P11D And Benefits Reporting Deadline

If you do not payroll benefits, you must file P11D forms and P11D(b) by 6 July 2026 where reporting expenses and employee benefits is required.

This deadline matters for:

- Reporting benefits in kind

- Class 1A National Insurance liabilities

- Year-end reporting for expenses and benefits

You can read more about HMRC requirements for benefits on the official GOV.UK expenses and benefits reporting page.

5 July 2026: PSA Application Deadline

If you want to set up a PAYE Settlement Agreement for the tax year, the application deadline is 5 July 2026.

Small Employers' Relief And Statutory Payment Recovery

Small Employers' Relief remains important for eligible employers reclaiming statutory payments.

From 6 April 2026, the compensation rate for Small Employers' Relief rises from 8.5% to 9%. This means qualifying employers can reclaim 109% of certain statutory payments from HMRC.

Eligibility depends on the employer’s Class 1 National Insurance position for the previous tax year. Employers should check HMRC guidance and confirm the position before making a reclaim through the EPS.

Legislative Changes From April 2026

April 2026 brings several changes employers should build into payroll planning.

National Living Wage Increase From 1 April 2026

The National Living Wage rises to £12.71 per hour from 1 April 2026 for workers aged 21 and over.

This change affects budgeting, payroll settings and compliance checks. Employers should review hourly rates, salary sacrifice arrangements and any workers close to the legal minimum.

You can check the official rates on the GOV.UK National Minimum Wage and National Living Wage rates page.

Statutory Sick Pay Changes From 6 April 2026

From 6 April 2026, Statutory Sick Pay is available to eligible employees regardless of earnings, because the Lower Earnings Limit has been removed. SSP is also payable from the first full day of sickness absence instead of after a waiting period.

Employers should update payroll software, absence rules and internal guidance before the first pay period of the 2026/27 tax year.

For official guidance, see the Business.gov.uk guide to Statutory Sick Pay changes.

Day 1 Rights For Paternity And Unpaid Parental Leave

From 6 April 2026, Paternity Leave and unpaid parental leave become Day 1 rights. Payroll professionals should make sure payroll systems and HR processes reflect this change, especially where leave affects statutory payment rates, scheduling or employee communications.

Payrolling Benefits And Benefits Reporting

Benefits compliance is another key deadline area for the 2026/27 tax year.

Voluntary Payrolling Registration Deadline

Employers that want to voluntarily payroll benefits for the 2026/27 tax year must register by 5 April 2026. After that date, the registration service closes for the year.

HMRC has confirmed that mandatory payrolling of benefits in kind is planned from April 2027, with exceptions for loans and accommodation benefits.

For more detail, see GOV.UK guidance on mandatory payrolling of benefits in kind.

Data Checks For Benefits In Kind

Before year-end reporting, employers should check:

- Benefit values and classifications

- Private medical and car benefit data

- Payroll benefits processed through payroll

- Class 1A National Insurance calculations

- Whether benefits will be filed through P11D reporting or payrolled

Payroll Software And Start-Of-Year Settings

A smooth start to the new tax year depends on solid payroll software preparation.

Before the first pay period after 6 April 2026, employers should:

- Install payroll software updates

- Review payroll settings and payment dates

- Apply HMRC tax codes or P9X carry-forward rules

- Check National Insurance thresholds and category letters

- Confirm student loan plans

- Review statutory payment rates

- Test BACS or Faster Payments processes where relevant

For smaller employers reviewing their systems, our Ultimate PAYE Guide for Small Business Payroll explains the core payroll process in more detail.

Student Loans, State Pension And National Insurance Changes

The start of the new tax year is also the right time to review employee-specific settings.

State Pension Age Checks

Identify employees approaching State Pension age so the correct National Insurance category letter is used. Once an employee reaches State Pension age, employee National Insurance treatment changes.

Student Loan Changes

Check student loan plan changes for the 2026/27 tax year before the first pay period. Incorrect plan settings can lead to over- or under-deductions and create correction work later.

Threshold And Rate Reviews

Review:

- Lower earnings limit

- National Insurance thresholds

- Income Tax settings

- National Insurance contributions treatment

- Any transitional protections that may affect individual employees

Making Tax Digital, Tax Avoidance And Wider Compliance

Payroll sits inside a wider compliance framework.

Making Tax Digital

Making Tax Digital for Income Tax starts on 6 April 2026 for those earning over £50,000. This is not a direct payroll deadline for every employer, but it may affect owner-managed businesses, sole traders on payroll and wider tax digital planning.

You can read more from AccountingPreneur on getting ready for Making Tax Digital.

Tax Avoidance Schemes

Employers should stay alert to PAYE tax avoidance schemes that promise lower liabilities through unusual salary structures or offshore arrangements. If something looks aggressive or unclear, get advice before processing it.

Recordkeeping And Compliance Evidence

To support compliance, employers should retain:

- Payroll reports and audit logs

- FPS and EPS confirmations

- P32 reports

- Bank payment evidence

- Approval records for corrections

- Benefits and expenses support

- Payroll records for the statutory retention period

Internal Cut-Offs, Bank Holidays And Payment Timing

The HMRC deadline is only one part of the process. Internal timing matters just as much.

Employers should set cut-off dates before each payroll run for:

- Timesheet approval

- Overtime and expenses

- Starter and leaver processing

- Absence updates

- Final payroll review

- Bank file release

Bank holidays can delay BACS and Faster Payments. Where payday falls near a holiday, move internal deadlines earlier and confirm the payment date still supports the FPS on-or-before rule.

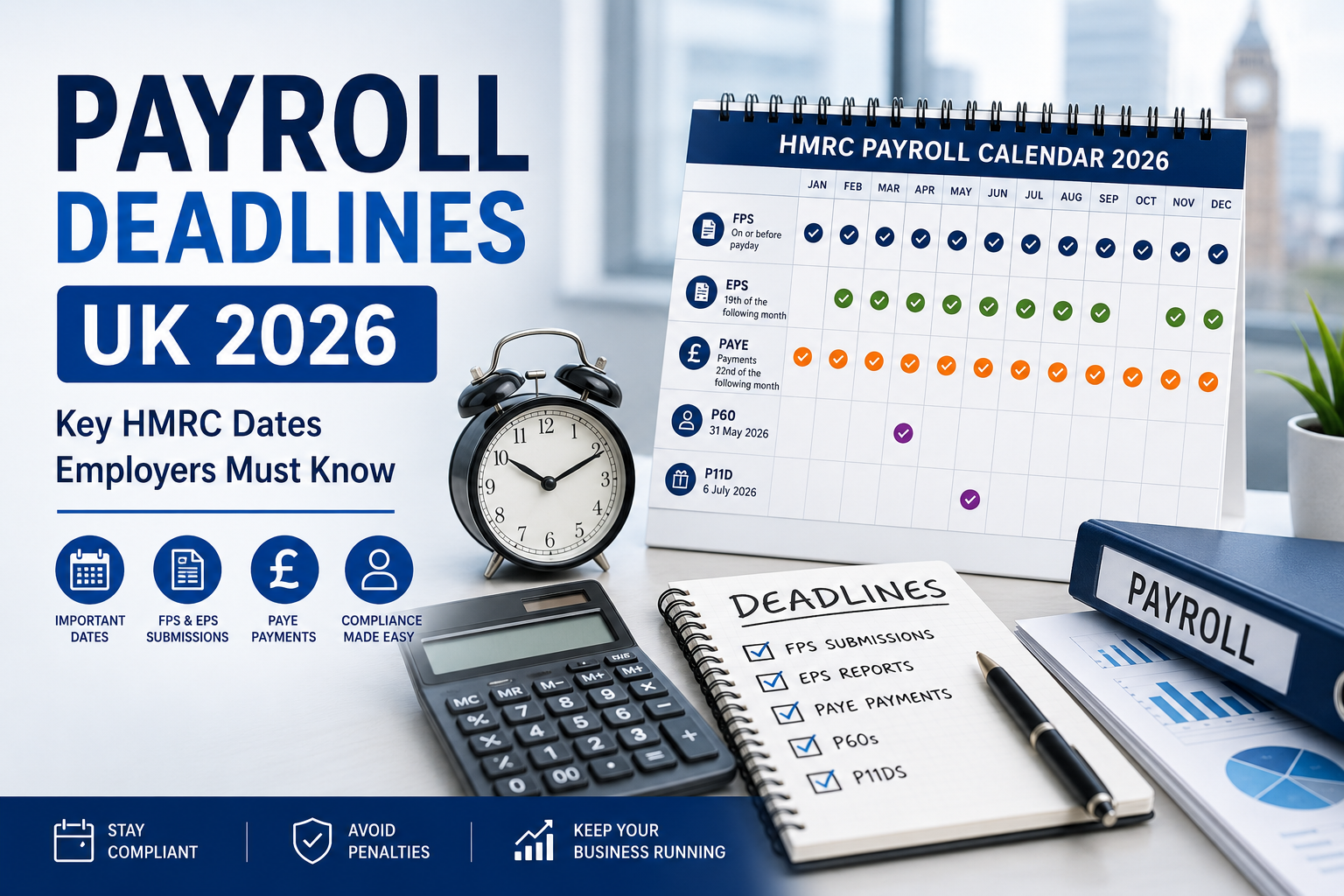

Calendar Of Key HMRC Payroll Dates For 2026

Here is a simple payroll calendar to add to your working plan.

Core Annual Dates

- 1 April 2026: National Living Wage rises to £12.71

- 5 April 2026: End of the 2025/26 tax year

- 5 April 2026: Deadline to register for voluntary payrolling of benefits for 2026/27

- 6 April 2026: Start of the 2026/27 tax year

- 19 April 2026: Deadline to send final EPS where required and finalise year-end RTI position

- 31 May 2026: Deadline to issue P60s to employees employed on 5 April

- 1 June 2026: Give benefits information to employees where needed

- 5 July 2026: PSA application deadline

- 6 July 2026: P11D and P11D(b) deadline for reporting expenses and benefits

- 22 October 2026: Electronic payment deadline for PAYE Settlement Agreement tax and Class 1B National Insurance

Recurring Monthly Dates

- On or before each payday: Submit FPS

- 19th of the following month: Submit EPS where needed, including no-pay EPS

- 22nd of the following month: Pay PAYE and National Insurance if paying electronically

Final Checks, Corrections And Recordkeeping

After final year-end submissions, employers should carry out a final review.

Reconciliation Steps

- Total pay against payroll reports

- PAYE due against the P32

- National Insurance payments and liabilities

- Statutory payment recoveries

- Benefits reporting position

- Leavers and starters across the tax year

Correction Controls

- Document the issue clearly

- Record the date and impact

- Keep approver evidence

- Retain revised reports and payment evidence

- File amended submissions where necessary

Retention Periods

In the UK, employers should generally retain payroll records for at least 3 years from the end of the tax year they relate to.

Final Thoughts

The payroll deadlines UK employers need to know in 2026 are not difficult to manage if your calendar, payroll software and internal controls are aligned. The pressure usually comes from late data, missed approvals, outdated settings or confusion around year-end steps.

Start with the fixed dates: 5 April 2026, 6 April 2026, 31 May 2026, 6 July 2026 and the 22nd of each month for electronic PAYE payments. Then build your internal process around the FPS on-or-before rule, the correct use of the EPS and the legislative changes taking effect from April 2026.

If you want help staying on top of deadlines, reducing risk and keeping payroll fully compliant, visit our payroll services page to see how we can support your team.

Get in touch today to see how we can help you!

Contact us

.png)

-min.png)

.png)